Insurance also allows you to compensate for damage caused by you to other people (for example, a traffic accident in which you are at fault). This type of damage is covered by compulsory and voluntary motor vehicle liability insurance.

Compulsory motor third party liability insurance

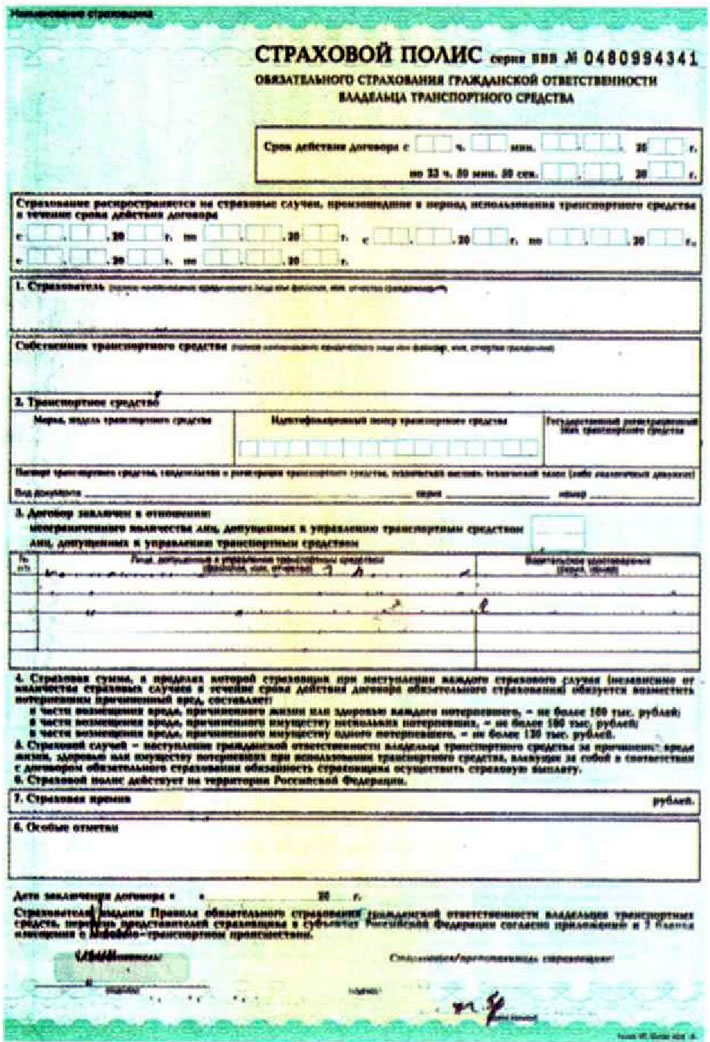

According to the Traffic Regulations, drivers of all motor vehicles registered in the established manner by the State Traffic Safety Inspectorate must have a valid Compulsory Motor Liability Insurance (OSAGO) policy.

The MTPL policy is included in the list of documents that every driver must have with him when driving a car.

This policy provides compensation for property damage caused by you in the amount of up to 120 thousand rubles (the only victim), up to 160 thousand rubles (several victims) and up to 160 thousand rubles in case of harm to health caused by you (to each victim).

The cost of an MTPL policy depends on the region where the car is registered, the engine power of the car and its category, the age category of persons permitted to drive the car, as well as their driving experience and accident-free driving experience. In case of accident-free driving during the previous year, the policyholder receives a discount of 5% of the cost of the policy being issued. This discount can reach 50%. In the future, when applying for subsequent policies for other cars, the discount can accumulate. However, in order to receive a discount, the persons admitted to management must remain unchanged.

The discount for accident-free driving is also retained in the case of insurance with another company, however, in this case you may be required to provide a certificate of accident-free driving from the company that previously issued the MTPL. The company is obliged to issue you this certificate. But some companies may, at their discretion, provide discounts based on just your application, written in simple written form. Be sure to save all previous MTPL policies, they may be useful for calculating the cost of the policy profitably.

Please remember that incorrect information about the vehicle and persons authorized to drive it provided by the policyholder may be grounds for penalties against the policyholder and, accordingly, an increase in the cost of the policy. In addition, in the event of a road traffic accident (RTA), information about accident-free driving is checked without fail, and if the fact of a previously committed RTA is revealed, the insurance company may refuse to pay out OSAGO, while returning the received insurance premium.

As a rule, the MTPL policy is issued for a period of one year. This is the most profitable. If the policy is issued, for example, for six months, then the cost of the policy will be 70% of the cost of the annual policy. If you subsequently renew your MTPL policy, you will only have to pay the remaining 30% of the cost of the annual policy.

When expanding the list of persons permitted to drive a car, the cost of the policy may increase taking into account the categories (age, experience) these persons.

In case of early termination of the MTPL contract, the policyholder is paid an amount equal to the remaining unspent amount minus 23% of the cost of the unspent amount.

Voluntary motor third party liability insurance

Voluntary motor third-party liability insurance (CTP) differs from CTP in the non-mandatory nature of its availability and the amount of insurance payments. DoSAGO does not cancel the presence of a valid OSAGO policy, but is only an addition to it, allowing you to increase the amount of insurance payments.

As a rule, when issuing a DoSAGO policy, a deductible is set (unpaid amount), covering payments under compulsory motor third party liability insurance. The deductible reduces the cost of insurance, but at the same time the cost of insurance payments also decreases.

Casco

Casco (translated from German as "vehicle") is a term used in insurance, denoting comprehensive voluntary insurance of a vehicle against various types of property damage. The risk insurance contract may include insurance against fire, natural disasters, theft, and damage to the vehicle (both due to the fault of the car owner and due to the fault of other persons).

The cost of CASCO may depend on the list of risks included in the insurance contract, the make of the car (in this case, the market value of the car and its theft rate are taken into account), driving experience and age category of persons permitted to drive, the presence of various anti-theft devices on the vehicle, the location of the vehicle storage (for example, a parking lot or a garage) and the presence of previously occurring insurance events for the insured.

Just as in the case of DoSAGO, the CASCO agreement may stipulate the amount of the deductible.

However, a CASCO contract may have its drawbacks. For example, if an insured event occurs due to the theft of a car, you may be denied compensation if you do not submit a complete set of keys and documents for the car to the insurance company.

In any case, when drawing up insurance contracts, you should be careful and try to clarify for yourself all unclear aspects of the contract.

[For details, visit the website «CHEVYMAN.RU»]